This Week's Review

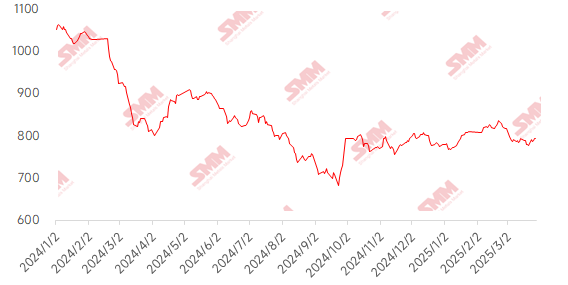

This week, iron ore prices fluctuated upward. At the beginning of the week, the Ministry of Finance released the 2024 fiscal policy implementation report, mentioning that the 2025 fiscal policy will be more proactive, boosting market sentiment. Fundamentally, port arrivals exceeded expectations, increasing by over 33% to reach a yearly high. Demand side, daily average pig iron production rose by 17,600 mt. Industrial data performed well, with apparent demand continuing to grow and total inventory destocking accelerating. Under these combined effects, iron ore prices continued to fluctuate upward this week. In terms of port prices, PB fines in Shandong rose by 10-15 yuan/mt MoM.

Chart: SMM 62% Imported Ore MMi Index

Data Source: SMM

Domestic ore prices rose slightly this week, and are expected to have further upside room next week.This week, prices in Tangshan, Qian'an, and Qianxi in Hebei increased by 10-15 yuan, while prices in west Liaoning, Chaoyang, Beipiao, and Jianping rose by 1-5 yuan/mt; prices in east China decreased by 1-5 yuan/mt.

Iron ore concentrate prices in Tangshan rose slightly, with 66% grade dry basis tax-included delivery-to-factory prices at 970-980 yuan/mt. Sentiment in mines and beneficiation plants was bullish, coupled with higher tender prices from steel mills, pushing market prices higher. Supply side, the market also found support, as volatile conditions led to thin or even negative profits for primary and secondary beneficiation, resulting in low operating rates and non-full-capacity or non-continuous operations. Local iron ore concentrate resources remained tight, providing some support to local prices. Demand side, pig iron production in steel mill blast furnaces continued to show an upward trend.

Steel enterprises in west Liaoning and surrounding areas have completed a new round of tenders, with current 66% grade wet basis tax-excluded iron ore concentrate prices at 720-730 yuan/mt. Traders and stockyards restocked as needed, and short-term market transactions improved. Iron ore futures adjusted, with buyer sentiment remaining cautious. Local steel mills currently have moderate production intentions, with no maintenance plans in the short term, which is expected to provide some support for local iron ore demand.

In east China, previously halted mines and beneficiation plants have not fully resumed production. Local mines and beneficiation plants sell as they produce, with no significant inventory pressure. It is expected that local iron ore concentrate resources will remain tight in the short term, and previously halted mines and beneficiation plants may gradually resume normal production in April.

Outlook for Next Week

For imported ore:Although steel mill profits have marginally narrowed, they remain resilient. Supported by the traditional peak demand season, major steel consumption is expected to continue to increase slightly, with total inventory maintaining a destocking trend. Steel mills are operating with low inventories and high production enthusiasm, and pig iron production still has upside room. Additionally, some steel mills' restocking demand before the Qingming holiday is expected to be released, potentially strengthening iron ore consumption and supporting ore prices. However, it is important to note that the unresolved crude steel production restriction policy continues to disturb the market, and the new US tariffs on China, effective April 2, are exacerbating risk-off sentiment. The upcoming contract rollover of the most-traded contract may amplify futures market volatility. Overall, iron ore prices are expected to continue fluctuating upward next week, but policy uncertainty may limit the upside room.

For domestic ore:Overall, domestic iron ore concentrate resources remain tight, providing some support to prices. Demand side, pig iron production in steel mill blast furnaces continues to show an upward trend, and domestic iron ore concentrate prices are expected to have some upside room in the short term.

Click to view the SMM Metal Industry Chain Database

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)